Introduction

In Sweden, loyal home insurance customers faced premium increases 6–10% higher than the market average — with no change in their underlying risk profile. The pattern is consistent across the Nordic region and beyond: in the UK, 6 million policyholders overpaid by ca. 10,4 milliarder DKK in 2018 through "price walking" — insurers systematically raising premiums on customers who simply stay. Pricing opacity, not coverage gaps, is the core problem.

Insurance costs rarely spike all at once. They creep up through auto-renewals accepted without question, duplicate policies nobody notices, and loyalty penalties that compound quietly year after year. This article breaks down the specific AI features — policy analysis, market comparison, and ongoing cost monitoring — that give consumers real visibility into what they're paying and why.

Key Takeaways

- Insurance costs build gradually through automatic renewals, duplicate coverage, and loyalty-based price increases

- Information asymmetry and deliberate policy complexity let insurers overcharge long-term customers

- AI software pinpoints coverage gaps, duplicate policies, and overpriced premiums you're already paying

- The biggest savings come from continuous oversight, not one-time switching

How Insurance Costs Quietly Build Up for Consumers

Insurance costs accumulate in a compounding pattern. Each year a policy auto-renews, the baseline for the next increase rises slightly—and consumers rarely revisit whether the coverage still fits their actual situation. This creates a silent erosion of value: paying more for the same (or less) coverage over time without a clear signal that something has changed.

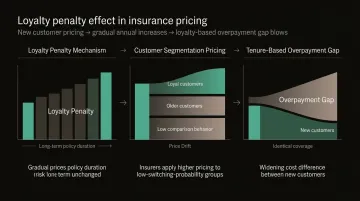

The Loyalty Penalty Phenomenon

The "loyalty penalty" is a documented pattern in insurance markets, not marketing myth. Research from Sweden's financial regulator shows that customers with the longest policy duration faced premium increases 6-10% higher than average for home insurance, despite customer loyalty having no impact on the risk of damages occurring. In Denmark, where the top five insurance companies control approximately 80% of the market, insurers systematically earn the most from loyal customers, customers aged 65 and over, and customers with shorter education—groups statistically less likely to shop around.

The mechanism is straightforward: insurers use complex pricing techniques to identify customers likely to renew without question, then increase their prices incrementally over multiple years.

By year ten, a loyal customer can pay 2,400 DKK more annually than a new customer for identical coverage. A premium that started at 4,800 DKK in year one can reach 7,200 DKK through tenure alone.

Duplicate Coverage Silently Adds Cost

In European travel insurance markets, 97% of premiums collected via bancassurance come from multi-trip policies, indicating a high risk of overlapping coverage with credit cards that already include travel protection.

Most insurers report that assessing overlap between policies is not part of the sales process. Consumers routinely pay for the same protection twice without realizing it.

This is not limited to travel insurance. Duplicate protections commonly appear across:

- Home and contents policies held with different providers

- Accident insurance bundled into employer benefits and private policies

- Liability coverage embedded in family plans and standalone policies

One Danish consumer using Inzure discovered she had been paying for duplicate travel insurance across two policies for years. The cost disappeared the moment it was identified.

Coverage Gaps Create Hidden Costs

Underinsured consumers face out-of-pocket expenses during claims that they believed were covered. In travel insurance, around 70% of insurers exclude pre-existing medical conditions from standard cover, often without pre-contractual medical screening. The main reason for denied travel insurance claims is exclusions in cover, raising questions about whether consumers received adequate information during the sales process.

One 86-year-old Danish consumer discovered she had been without home contents insurance for at least 10 years. That gap exposed her to serious financial risk every day she went without it. These are the costs that never show up on a premium statement—until something goes wrong.

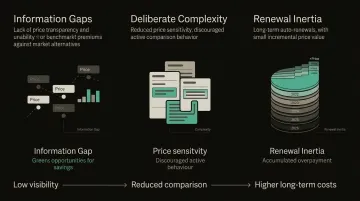

Key Cost Drivers Behind Inflated Insurance Premiums

Information Asymmetry Is the Foundational Driver

Insurers have full visibility into pricing logic, claims data, and competitive positioning. Consumers lack tools to assess whether what they pay is fair relative to the actual market rate. This asymmetry is structural, not incidental. When one neighbour pays 4,800 DKK annually for home insurance while another pays 8,300 DKK for identical coverage in the same postal code, the difference has nothing to do with risk — it comes down to who has better information.

Policy Complexity Is Deliberate

The harder a policy is to understand or compare, the less likely a consumer is to question it or shop alternatives. This is a documented strategic pattern. According to EIOPA's Consumer Trends Report, 71% of consumers find insurance policies have vague terms and unclear coverage — and the same share report that technical jargon makes documentation difficult to parse.

Insurance companies design 32-page policy documents that are never meant to be read. Complexity reduces price sensitivity and makes comparison across providers genuinely difficult. In Denmark, households spend an average of nearly 16,000 DKK annually on non-life insurance — a figure that reflects how effectively opacity suppresses comparison shopping.

Timing and Inaction Drive Cost

Complexity doesn't just confuse — it exhausts. Consumers who accept the default renewal without reviewing terms or comparing prices consistently overpay, regardless of coverage type or provider. The European Insurance and Occupational Pensions Authority (EIOPA) has explicitly warned against "price walking" practices — repeatedly increasing prices at renewal based on low propensity to shop around or low price elasticity — as leading to unfair treatment and non-compliance with insurance distribution regulations.

Three patterns consistently inflate what Danish households pay:

- Information gaps — consumers can't assess whether their premium is fair without market data

- Deliberate complexity — dense policy documents reduce price sensitivity and discourage comparison

- Renewal inertia — insurers exploit low switching rates through incremental price increases year over year

How AI Software Helps You Reduce Insurance Costs

Most Danish households overpay on insurance not because they made a bad decision once, but because nothing prompts them to revisit it. AI changes that — across three distinct pressure points: what you buy, how you manage it, and how you negotiate.

Strategies That Reduce Costs by Changing What You Buy

AI enables smarter coverage decisions before or at the point of purchase, eliminating the assumption that more coverage always means better value.

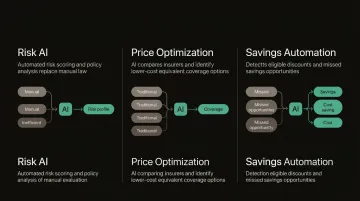

Identify redundant or overlapping coverage using AI-powered policy analysis

AI can read across all your existing policies and flag where two or more policies cover the same risk. This allows consumers to eliminate duplicate premiums they are already paying, often for years without realizing it. Platforms like Inzure analyze uploaded policy documents in under 60 seconds, surfacing overlaps such as duplicate travel insurance held through both a credit card and a standalone policy.

Right-size coverage to actual need

AI tools compare what a policy covers against a consumer's actual risk profile, identifying expensive coverage features that are unlikely to affect them. This helps consumers make a conscious trade-off rather than defaulting to maximum coverage. For example, one Danish family discovered their newborn was being charged for coverage when the child should have been included free until age two, an unnecessary cost that AI analysis caught instantly.

Check real market benchmarks before renewing

Rather than accepting the renewal price as a given, AI software surfaces what comparable coverage actually costs on the open market. This turns a routine renewal into an informed negotiation or switching decision. When consumers know their 7,200 DKK home insurance renewal is 38% above the market rate, they can act rather than accept.

Strategies That Reduce Costs by Changing How You Manage Coverage

Ongoing oversight powered by AI eliminates the cost that accumulates between decisions, particularly the annual auto-renewal drift that goes unnoticed.

Automate policy monitoring for price changes and coverage shifts

AI tools that continuously track your insurance portfolio can alert consumers when:

- Premiums increase beyond a threshold

- Coverage terms silently change at renewal

- A better-priced equivalent appears in the market

Without AI oversight, consumers only review insurance after a life event (house purchase, new car) or after a price shock. Continuous monitoring catches problems early, before overpayment has already compounded.

Conduct a full policy audit in minutes rather than hours

Traditionally, reviewing and cross-referencing multiple insurance documents required significant time and expertise. AI-powered platforms can now analyze a full household insurance portfolio in under 60 seconds, surfacing issues that would otherwise stay hidden for years.

Inzure offers consumers a complete analysis of their policies, covering coverage gaps, duplicates, and real market pricing data, with no obligation to switch. What once took 10 hours of manual comparison now takes one minute of automated analysis.

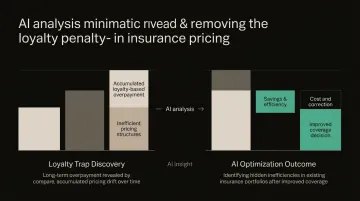

Eliminate the loyalty trap

One Danish consumer saved 48,000 DKK annually (a 46% reduction) after eight years with the same insurer, not by cutting coverage, but by identifying how much the loyalty penalty had compounded over time. Another saved 2,800 DKK annually while simultaneously adding a fourth policy to cover a critical gap discovered through AI analysis. These are not edge cases; they reflect the systematic overcharging that AI makes visible.

Strategies That Reduce Costs by Changing Your Market Position

AI changes the power dynamic between consumers and insurers by giving consumers the market context and data confidence they have historically lacked.

Understand real market pricing before any conversation with an insurer

AI platforms that aggregate and benchmark pricing data allow consumers to enter renewal conversations knowing what the actual market rate is. This shifts the negotiating position from passive to informed. When you know your current premium is 4,600 DKK above market, you have leverage.

**Reduce the friction of switching providers**

Insurers rely on complexity to retain customers at inflated prices. AI removes that barrier by:

- Comparing coverage across multiple providers in plain language

- Translating dense policy terms so trade-offs are immediately clear

- Quantifying the cost-benefit of switching in concrete numbers

Rather than spending hours decoding 32-page policy documents, consumers see a direct summary: "You are paying 35% above market for identical coverage."

Turn AI-identified savings into a clear prompt for action

When AI analysis surfaces a specific, quantified gap, such as "you are paying 38% above market rate for your home insurance," it creates an immediate reason to act. Vague awareness rarely moves people. A precise number does.

Conclusion

Reducing insurance costs is not primarily about cutting coverage—it is about understanding where cost originates. Danish consumers consistently overpay because insurers hold all the information — pricing logic, comparable market rates, renewal inflation. AI software closes that gap by making policy analysis, market comparison, and ongoing oversight accessible in minutes rather than months.

The consumers who save the most are not those who switch once and forget it. They replace annual inertia with continuous oversight — catching price increases, spotting duplicate coverage, and comparing the market whenever their situation changes. The insurance industry was built to make this difficult. AI makes it straightforward.

Frequently Asked Questions

How can insurance AI software help reduce costs?

AI software reduces insurance costs by analyzing existing policies for duplicates, gaps, and pricing misalignment. It then surfaces real market rates so consumers can make informed decisions rather than defaulting to auto-renewal — eliminating hidden loyalty penalties and unnecessary coverage.

How is AI used in insurance pricing?

On the insurer side, AI handles risk scoring and predictive modeling to calculate premiums. Independent consumer-facing tools take a different approach — they benchmark your current premium against live market pricing to reveal whether you're overpaying for your actual risk profile.

What can AI do for insurance companies?

For consumers, independent AI platforms analyze policy documents to identify coverage gaps, duplicate policies, and price misalignment across carriers. Rather than replacing your insurer, these tools give you the market transparency needed to negotiate better terms or switch to a more competitive provider.