Introduction

Most people sign an insurance policy and never look at it again — insurers are counting on exactly that. Dense legal language, hidden exclusion clauses, and renewal letters that quietly bury price increases are deliberate design choices — ones that serve the insurer, not you.

The consequences are real: you might overpay for years without realizing it, only discovering coverage gaps when a claim is denied, or paying for duplicate policies across home contents, travel, or accident insurance. Manually reviewing and comparing policies takes 10+ hours per policy. Most consumers never do it.

This guide covers what AI-driven insurance data analysis is, how it works step by step, what it can uncover, and how tools using this technology are handing the power back to consumers. If you've ever felt frustrated by insurance jargon or uncertain whether you're getting a fair deal, this guide gives you the tools to find out.

Key Takeaways

- Automatically reads and decodes your insurance policies to show what you're paying for and whether the terms are fair

- Transforms manual comparison (10+ hours) into under 60 seconds

- Detects coverage gaps, duplicate coverages, price increases, and benchmarks your premium against market rates

- Works across home, travel, accident, liability, and family insurance plans across all Danish insurers

- Gives you clear, actionable insight to make confident decisions about your coverage

What Is AI-Driven Insurance Data Analysis?

AI-driven insurance data analysis uses artificial intelligence — including natural language processing (NLP), machine learning, and document-reading models — to automatically extract, interpret, and evaluate insurance policies on your behalf.

Instead of spending hours manually reading dense policy documents, AI does this work in seconds, translating complex legal language into clear answers you can act on.

Where and How It Applies:

This technology isn't limited to one insurance type. The same AI reads policies across all common personal insurance categories — extracting coverage terms, exclusion clauses, premium amounts, renewal conditions, and price change history. That includes home (indboforsikring), travel (rejseforsikring), accident (ulykkesforsikring), liability (ansvarsforsikring), legal aid (retshjælp), and bicycle theft (cykeltyveri).

Two Main Approaches:

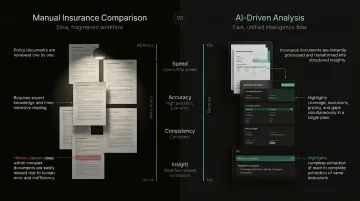

- Manual comparison: Slow, error-prone, and requires expert knowledge most consumers don't have — so it rarely gets done at all

- AI-driven analysis: Completes the same review in under 60 seconds, consistently, without needing any prior insurance knowledge

In practice, manual comparison might take 10 hours per policy and still miss exclusion clauses buried on page 14. AI catches exactly what humans overlook — every time.

Why AI Insurance Data Analysis Matters for Consumers

The Insurance Market Is Structurally Opaque

Policies are written in dense legal language, renewal letters downplay price increases, and loyalty to a single insurer typically results in steadily higher premiums rather than rewards.

According to GDPR guidelines governing insurance data processing, insurers handle vast amounts of personal data — yet consumers rarely have the tools to understand what they're actually buying or whether they're getting fair value. The system is designed to favour insurers, not policyholders.

Coverage Gaps Are Invisible Until It's Too Late

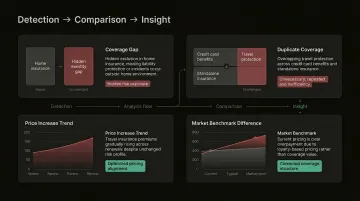

Coverage gaps stay hidden until a claim is rejected — and by then, the damage is done. AI can identify missing coverage categories — such as no personal liability cover, no water damage clause, or no coverage for family members — before a crisis exposes the gap. One Inzure customer discovered his partner wasn't listed on their home, accident, or travel insurance policies, leaving half the household unprotected for years.

Duplicate Coverage Is Common and Costly

Consumers with multiple policies — car, home, travel, contents — frequently pay for overlapping coverage. Travel cancellation protection, for example, might appear in both a standalone travel policy and a credit card benefit. Common duplicates include:

- Personal liability covered under both home and travel policies

- Accidental damage appearing across contents and standalone accident cover

- Legal aid included in multiple product bundles

AI detects when the same risk is covered twice and calculates the unnecessary spend, so you can drop redundant coverage and keep the savings.

Price Benchmarking Reveals the Real Market Value

AI compares a consumer's current premium against what the same coverage would cost with alternative providers, making it immediately visible when someone is paying above-market rates. Loyal long-term customers often pay significantly more than new customers for equivalent coverage — a practice known as loyalty pricing. Inzure customers have discovered they were paying 24% to 46% above market rates, with annual overpayments ranging from DKK 2,800 to DKK 48,000.

AI Does the Research in 60 Seconds

Researching, comparing, and understanding insurance policies manually can take many hours per policy. AI compresses that process into 60 seconds, removing the single biggest reason consumers avoid reviewing their coverage regularly. That time saving alone is why most people who try an AI analysis do it more than once.

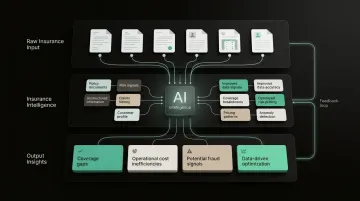

How AI Insurance Data Analysis Works – Step by Step

Understanding what happens at each stage makes it easier to act on the findings — and to see why the analysis catches things a manual review never would. Here's how the process works:

Step 1 – Upload Your Policy Documents

The consumer provides their existing insurance documents — typically a PDF, a scanned copy, or a photo taken on a phone. No specialist knowledge is required: the AI accepts documents as issued by the insurer, regardless of format or provider.

A good system accepts policies from any Danish insurer without pre-formatting — no manual data entry needed.

Step 2 – Data Extraction and Document Reading

The AI uses optical character recognition (OCR) and natural language processing (NLP) to read the full policy document — every clause, condition, exclusion, and renewal term, including the fine print buried on page 14 that most people skim or miss entirely. Exclusion clauses hidden deep in the document are precisely where the analysis adds the most value.

Step 3 – Structuring and Categorising the Data

Raw extracted text is cleaned, classified, and organised into structured categories:

- Coverage types

- Coverage limits

- Exclusions

- Premiums and payment terms

- Renewal conditions

- Price change history

This step makes policies from different insurers comparable side by side, even when they use different terminology or document layouts.

Step 4 – Running the Analysis

The structured data is run through the AI's analytical models:

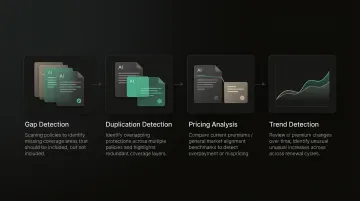

- Gap detection: What should be covered but isn't?

- Duplication detection: What's covered by more than one policy?

- Pricing analysis: Is the premium in line with market benchmarks?

- Trend detection: Has the premium increased significantly at recent renewals?

AI trained across many insurers and policies detects patterns that no individual consumer could spot on their own.

Step 5 – Interpreting and Presenting Results

The analysis is translated from technical findings into plain-language recommendations:

- "Your home insurance doesn't cover water damage from burst pipes"

- "Your travel policy duplicates your credit card's travel cover"

- "Your contents insurance (indboforsikring) premium is 38% above the current market average"

The quality of this step determines whether someone acts on the findings — specific, plain-language output drives real decisions.

Step 6 – Act on the Insights

The consumer uses the insights to decide: negotiate with their current insurer, switch to a better-value provider, drop duplicate coverage, or add missing coverage before they need it.

Premiums and market rates shift annually, so reviewing the analysis periodically keeps savings current. The most value comes from treating it as an ongoing monitoring tool, not a one-time check.

AI Insurance Data Analysis – A Real-World Example

Consider a Danish consumer who has held home insurance (indboforsikring) and travel insurance (rejseforsikring) with the same provider for seven years, auto-renewing both annually without reviewing the terms or comparing prices. They've never read beyond the first page of their policy documents and assume their insurer is treating them fairly because they've been loyal customers.

The Analysis Process:

Document upload takes seconds — both policies uploaded as PDFs. The AI reads both full policies, including every exclusion clause and coverage limit. Within 60 seconds, the analysis is complete.

What the AI Discovers:

- Coverage Gap: The home insurance excludes personal liability for incidents outside the home. If a family member accidentally damages a neighbour's property or causes an injury away from home, there's no coverage — the kind of gap that only surfaces when a claim is denied.

- Duplicate Coverage: The consumer has been paying for travel cancellation cover through both a credit card benefit and a standalone travel policy. Danish consumers typically pay DKK 500–800 annually for standalone travel cancellation that duplicates what's already included with premium credit cards.

- Price Increase: The travel insurance premium rose 28% over three renewals with no change in risk profile, coverage, or claims history. The insurer raised the price each year; the consumer never noticed because renewal letters framed the increase as routine.

- Market Benchmark: The combined premium sits 35% above the current market rate for equivalent coverage. This isn't because the policies are better — it's loyalty pricing. New customers switching to comparable providers pay significantly less.

The Outcome:

Armed with this analysis, the consumer contacts the insurer with market data, negotiates a reduction, or switches to a comparable provider at a lower premium. In this case, switching saved DKK 25,000 annually — a 35% reduction — while also closing the liability gap and dropping the duplicate travel coverage.

Inzure runs this exact analysis automatically. Upload your policies and get a full breakdown — coverage gaps, duplicates, price increases, and market benchmarks — in 60 seconds, free to use.

How Inzure Can Help

Inzure is Denmark's first AI-driven, independent insurance analysis platform — built specifically for Danish consumers, covering Danish insurers, and operating with full GDPR compliance and EU data storage. Unlike comparison sites tied to insurer partnerships, Inzure has no financial relationship with any insurer, meaning its analysis is independent.

What You Get in 60 Seconds

Upload your existing policies and receive a full analysis in under a minute. The analysis identifies:

- Gaps in coverage

- Duplicate policies

- Above-market pricing

- Price increases at renewal

All presented in plain Danish, without requiring any insurance expertise from the consumer.

A Pricing Model Built Around Your Savings

That analysis is just the starting point. Inzure is free to use — consumers only pay 20% of verified annual savings, and only if Inzure identifies a better deal. No obligation to switch, no hidden fees, no subscription. For anyone overpaying by thousands of kroner annually, the platform effectively pays for itself.

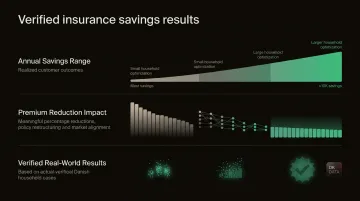

Inzure's customers have achieved savings ranging from DKK 2,800 to DKK 48,000 annually, with premium reductions between 24% and 46%. These are verified reductions from real Danish households — not projections.

Conclusion

AI-driven insurance data analysis doesn't require expertise, time, or technical knowledge from the consumer — it requires only that you give the AI access to what you're already paying for. In return, it shows you whether your coverage is complete and whether you're paying a fair market price.

Insurance premiums change, personal circumstances evolve, and market rates shift. That makes AI analysis most valuable as an ongoing monitoring tool — a continuous safeguard against gradual overpayment and silent coverage erosion.

The consumers who benefit most treat it as an annual habit, ideally before each renewal. Used that way, it keeps you informed, keeps your coverage current, and keeps insurers accountable on price.

The practical starting point:

- Upload your current policy documents for an immediate gap and pricing check

- Set a reminder to re-run the analysis before your next renewal date

- Switch only if the savings justify it — there's no obligation to act

Frequently Asked Questions

What types of insurance policies can AI analyse?

Inzure analyses the personal insurance categories most Danish households hold: home (indboforsikring), travel, accident, liability, legal aid, and bicycle theft coverage. The platform reads policies from all Danish insurers regardless of format, so you don't need to prepare or reformat documents before uploading.

Is my data safe when I upload insurance documents to an AI platform?

Reputable AI insurance platforms operate under GDPR compliance with EU-based data storage, meaning your personal and policy data is protected under European data privacy law. Inzure stores all data on EU servers and does not share your information with any insurance company — your analysis stays yours.

How accurate is AI at reading and analysing insurance policy documents?

Modern AI using natural language processing and document scanning technology can read insurance documents with high accuracy, extracting coverage terms, exclusions, and pricing details that even experienced readers might miss. Accuracy improves when the full policy document is provided rather than just a summary or renewal notice.

Can AI insurance analysis actually tell me if I'm overpaying?

Yes. AI insurance analysis benchmarks your current premium against live market rates for equivalent coverage, showing you directly whether you're overpaying and by how much.

How is AI insurance analysis different from using a comparison website?

Comparison websites show you new quotes based on information you manually enter, whereas AI insurance data analysis reads your existing policies and identifies specific issues within them — including coverage gaps, duplicate policies, and overcharging — before recommending any action. The starting point is your actual policy, not a blank quote form you fill in yourself.

How often should I use AI to review my insurance policies?

At minimum, an annual review timed before renewal. You should also review after major life changes — moving home, getting a bicycle, having children — that shift your coverage needs. Continuous monitoring platforms like Inzure can also flag mid-year price changes or market shifts automatically.