Introduction

Imagine filing a claim for a stolen bicycle only to discover that your home insurance doesn't cover it—not because you chose to exclude it, but because that crucial clause was silently removed at last year's renewal. You assumed nothing had changed. The insurer never highlighted the modification. Now you're out of pocket, with no recourse.

This scenario is the predictable result of how insurance policies are structured and sold. These documents run to hundreds of pages, written in dense jargon that discourages careful reading. Most people sign once, file them away, and forget them until something goes wrong.

Insurers have little financial incentive to make these documents easy to review. Danish law permits premium increases of up to approximately 5% annually without advance notice. The result: errors, gaps, and silent cost increases that consumers discover only when it's too late.

That's where policy checking comes in. It's the process of reviewing your insurance documents to confirm that what you're paying for is accurate, complete, and still matches what you actually need — your primary defense against hidden risks you'd otherwise only find at claim time.

Key Takeaways

- Policy checking verifies your insurance accurately reflects what you agreed to and actually need

- Errors are far more common than most realize and often go undetected until a claim is denied

- A proper check covers limits, exclusions, deductibles, named insureds, duplicates, and premium accuracy

- Skipping a check risks paying for wrong coverage, missing critical protections, or facing claim denial

- AI tools now analyze policies in 60 seconds, making consumer-side policy checking practical for the first time

What Is Policy Checking?

Policy checking is the process of reviewing an issued insurance document against what was quoted, requested, and agreed upon — verifying that coverages, limits, exclusions, premiums, and policyholder details are all accurate and consistent with your needs.

The term covers two distinct practices. Insurers and brokers use it internally to validate documents before delivery. For consumers, it means reviewing your own policy at issuance and renewal to confirm it still matches your situation — and that's the focus here.

Policy checking is not a one-time task. It should happen:

- At every annual renewal

- After any major life change (moving home, getting married, having a child, adding a family member to your household)

- Whenever your insurer sends a policy update notice — even if it seems routine

The review typically involves comparing several documents: your original application, the quote you received, any mid-term changes or riders issued, and the final policy document itself. Errors hide in the gaps between these layers.

Why Policy Errors Are More Common Than You Think

Insurance policy documents are genuinely complex. A standard home or family insurance policy can run to 50–100 pages of legal terminology, fine-print exclusions, and nested clauses. That complexity breeds errors—both at the insurer's end (data entry mistakes, system transfer errors, incorrect form application) and on the consumer's side (assumptions about coverage that go unchecked).

The Comprehension Gap

Most consumers don't read their policies—and significantly overestimate their understanding. A 2026 Trusted Choice survey found that only 31% of consumers review their insurance policies annually, while 49% revisit coverage only after a premium increase—or never at all.

The knowledge gaps are striking. A 2024 Trusted Choice study found that 86% of consumers claim a "strong grasp" of their policies, yet 56% were unaware that standard homeowners policies exclude flood damage and 70% didn't know that renovation materials are excluded.

Academic research published in the Journal of Consumer Policy shows that readability of insurance contracts directly shapes consumer trust and expectations. Plain-language contracts produce more accurate expectations—but most policies are not written that way, and the gap between what consumers believe they're covered for and what they actually are remains wide.

Renewal: The Highest-Risk Moment

Renewal is when silent changes are most likely to slip through. Insurers may adjust terms, add exclusions, or increase premiums—often with minimal notification.

Under Danish law (Section 3b of the Insurance Contracts Act), insurers must provide at least 30 days' notice for "material changes" that disadvantage the customer. Yet the Danish Supreme Court has ruled that annual premium increases of 3.1%–3.8% (approximately 105 DKK per policy) are "insignificant"—meaning they don't trigger the notification requirement. Those incremental hikes compound year after year without any alert reaching you.

Without comparing this year's policy against last year's, these changes remain invisible.

The E&O Problem from the Consumer's Perspective

When a policy contains an error—wrong deductible, missing endorsement, incorrect insured name—and a claim is filed, insurers may use that discrepancy to reduce or deny payment. You bear the financial cost of an error you had no part in creating.

According to EIOPA's 2025 Flash Eurobarometer, among EU consumers dissatisfied with their claims experience, 20% cited "unclear policy terms led to an unexpected denied claim" and 23% said the payout amount was less than expected. These aren't edge cases—they're systematic outcomes of policy complexity and consumer inattention.

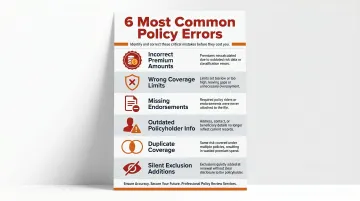

Most Common Policy Errors

The errors consumers most frequently encounter include:

- Incorrect premium amounts or unexplained increases

- Wrong coverage limits (especially underinsurance—more on this below)

- Missing or lapsed endorsements (e.g., bicycle theft, legal aid)

- Outdated policyholder information (old address, previous vehicle, former spouse still listed)

- Duplicate coverage across multiple policies (travel insurance via credit card and standalone policy)

- Silent exclusion additions at renewal

None of these announce themselves. You only find them when you look—or when a claim gets denied and it's too late.

What a Thorough Policy Check Should Cover

A comprehensive policy review isn't about reading every word on every page—it's about systematically verifying the elements that matter most. Here's what to check:

Policyholder and Property Information

Start with the basics. Confirm that all identifying details are correct:

- Full legal name of the insured (exactly as it appears on official documents)

- Address of the insured property

- Policy number and effective/expiration dates

- Named additional insureds (spouse, children, business partners)

Even a minor discrepancy—a misspelled name, an outdated address—can complicate or delay a claim.

Coverage Types and Limits

Verify you have the coverage types you actually requested. For home insurance, does the policy cover building and contents, or contents only? For accident insurance, does it include rehabilitation and dental care, or just lump-sum disability payments?

Then check the limits: the maximum the insurer will pay. Limits should reflect current replacement costs, not historical values. Underinsurance—setting limits too low—is more common than most policyholders realize.

Across Europe, the numbers are striking. Data from the UK shows that **70% of properties are insured below their true rebuild cost**, carrying on average only 66% of required cover. In Ireland, underinsurance rose from 6.5% to 16.5% between 2017 and 2022, driven by inflation and rising rebuild costs. Danish households face the same risk.

If your sum insured hasn't been updated in years, it's almost certainly too low.

Deductibles and Exclusions

Deductibles—the amount you pay before insurance kicks in—and exclusions—events or damages not covered—are two of the most misunderstood policy elements.

Confirm your deductibles match what you agreed to. A deductible that's crept from 2,500 DKK to 5,000 DKK without your knowledge can double your out-of-pocket cost on a claim.

Exclusions are equally critical. Check whether new exclusions have been added since last renewal. Common additions include exclusions for unoccupied homes, business use of personal vehicles, or specific types of water damage.

Endorsements and Add-Ons

Endorsements modify your base policy—they can add coverage (flood protection, valuable items rider, legal aid) or restrict it (business use exclusion, specific perils excluded).

Endorsements agreed upon at purchase must appear in the final document. Missing endorsements are a leading cause of unexpected claim denials.

If you requested bicycle theft coverage or legal aid insurance and it's not explicitly listed, you don't have it—even if you're paying for it.

Premium Accuracy and Duplicate Coverage

Verify that the premium you're being charged matches the quote. Discrepancies of even 100–200 DKK per year add up significantly over a decade.

Cross-check for duplicate coverage. Common examples:

- Travel insurance bundled with your credit card and purchased as a standalone policy

- Contents coverage included in a home policy that duplicates a separate renters policy

- Legal aid or accident coverage provided by multiple policies

Paying twice for the same protection is a silent cost that policy checking eliminates.

The Real Cost of an Unchecked Policy

The Claim-Denial Scenario

When you file a claim and discover a policy error or gap for the first time, it's too late to fix it. You either receive a reduced payout, a denied claim, or must pursue a costly dispute process—often with uncertain outcomes.

A case documented by Denmark's Insurance Appeals Board involved a consumer whose theft claim for over 900,000 DKK in cash and jewelry was initially denied by Tryg, which argued the home was not "properly locked." Both the Appeals Board and the court ultimately ruled against the insurer—but the consumer faced months of uncertainty and legal expense before recovering their claim.

In Ireland, the Central Bank found that for customers whose claims were reduced due to underinsurance, the average reduction was approximately 19% in 2021. If your house has a rebuilding cost of €200,000 but you're only insured for €100,000, a partial damage claim of €50,000 yields just €25,000. The remaining €25,000 comes out of your pocket.

The Loyalty Penalty

Loyal customers who renew without checking are systematically subjected to incremental premium increases year over year—a practice known as "price walking" or the "loyalty penalty."

Research by Denmark's Competition and Consumer Authority (Konkurrence- og Forbrugerstyrelsen) confirmed in April 2025 that loyal non-life insurance customers systematically pay more than new customers. According to Forbrugerrådet Tænk, customers who have been with the same insurer for 10 years typically pay approximately 100 DKK more per month—translating to over 5,000 DKK more per year—than new customers with identical coverage.

In the UK, the Financial Conduct Authority found that in 2018, 6 million loyal home and motor policyholders were paying a loyalty penalty, collectively overpaying by £1.2 billion. The pattern is cross-border and structural, not accidental.

The Psychological Cost

Beyond the financial impact, there's a harder cost to measure: the false sense of security that comes from believing your coverage is solid, only to find out it wasn't when you need it most. That erosion of trust is compounded by the fact that insurance complexity is rarely accidental. It is a deliberate feature of a system that benefits when consumers don't compare, don't question, and don't switch. Checking your policy regularly is one of the few tools consumers have to push back.

How AI Is Making Policy Checking Faster and More Accessible

Traditionally, thoroughly checking an insurance policy required either professional expertise (hiring a broker or advisor) or hours of careful reading and comparison. For most consumers, neither option was practical. AI has changed that — making comprehensive policy analysis fast, accessible, and affordable for ordinary households.

What AI Policy Checking Does

AI-powered policy checking tools use natural language processing (NLP) and machine learning to automate the extraction, comparison, and validation of policy data. They:

- Read the full policy document, including fine print and complex clauses

- Extract key fields: coverage types, limits, deductibles, exclusions, premiums, policyholder details, endorsements

- Compare extracted data against market benchmarks, prior policy versions, and expected values

- Flag discrepancies for review: missing coverage, duplicate policies, premium inflation, exclusions added at renewal

McKinsey reports that insurers are building integrated product repositories that allow agents to use NLP to query coverage details and exclusions in real-time. Deloitte documented the application of NLP-based AI to analyze over 300,000 insurance policies, achieving "near 100% accuracy for all extraction quantities."

What previously took 10+ hours can now be completed in 60 seconds.

The Consumer-Side AI Revolution

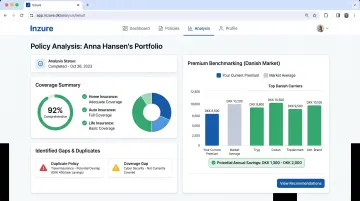

Those same capabilities are now available directly to consumers. Inzure is Denmark's first independent, AI-driven insurance platform built specifically for households — analyzing policies without affiliation to any insurance company, working exclusively for the customer.

The platform allows users to upload their policy documents (PDF or photo) and receive a comprehensive analysis within 60 seconds. The AI identifies:

- Missing coverage: Common gaps like bicycle theft, legal aid, or family-member exclusions

- Duplicate policies: Travel insurance already covered by credit cards, overlapping contents coverage

- Premium inflation: Loyalty surcharges and unjustified annual increases

- Underinsurance: Sum insured below current replacement costs

Inzure benchmarks each policy against real-time Danish market data across major carriers (Tryg, Alka, Topdanmark, Codan, GF, Alm. Brand, and others), highlighting where customers are overpaying or underprotected.

The revenue model is straightforward: the analysis is free. Inzure charges a 20% commission on savings only if the customer switches and achieves actual cost reduction. If a switch delivers better coverage at the same price, there's no fee. All data is GDPR-compliant and stored within the EU.

Early users have reported savings ranging from 2,800 DKK to 48,000 DKK per year by identifying and correcting errors insurers never disclosed.

Consumer Trust in AI

According to EIOPA's 2025 Eurobarometer, 30% of EU consumers would trust recommendations from non-human AI agents when choosing insurance or pension products. While trust is not yet mainstream, it's growing—and the practical benefits of AI-driven policy checking are accelerating adoption.

The global InsurTech market is projected to grow from $23.54 billion in 2026 to $132.71 billion by 2034, at a compound annual growth rate of 24.1%. For Danish consumers navigating carriers that rarely volunteer comparisons or flag overpayments, AI-powered analysis has shifted from a novelty to a practical first step.

Frequently Asked Questions

What is policy checking?

Policy checking is the process of reviewing an issued insurance document to confirm it accurately reflects the coverage, limits, premiums, and terms agreed upon. It can be done by insurance professionals or by consumers reviewing their own policies.

What is AI for insurance policy checking?

AI for insurance policy checking uses machine learning and natural language processing to automatically read, extract, and compare data across policy documents, flagging errors, coverage gaps, duplicates, and price discrepancies far faster and more accurately than manual review.

How can I check my insurance policy status?

You can check your policy status by logging into your insurer's online portal or contacting your broker directly. Independent AI-powered platforms like Inzure can also analyze your full policy document and summarize current coverage, limits, and any issues.

Can you look up an insurance policy online?

Many insurers provide online portals where policyholders can view current policy documents. Independent platforms can also access and analyze policy documents you upload, offering a more detailed and unbiased review of coverage.

Do insurance companies do checks?

Insurers conduct their own internal underwriting checks, but these are designed to protect the insurer's risk—not to verify that you received what you paid for. Independent policy checking, either manually or through consumer-facing AI tools, is an essential additional step for policyholders.