This article is for Danish consumers using comparison platforms to find better insurance deals. We'll clarify how these services actually verify quotes, why the price you see isn't always the price you get, and what structural limitations affect the accuracy of every comparison result you receive.

Key Takeaways

- Comparison quotes are estimates, not binding prices. Final costs are confirmed only after underwriting.

- Quote accuracy depends on complete, honest user data and real-time insurer pricing

- No comparison platform covers 100% of the Danish market — Forsikringsguiden reaches 86% of insurers by premium volume, missing 14%

- Many platforms earn commissions from insurers, creating bias toward specific results

- Final premiums often differ from initial quotes once insurers run credit checks, claims databases, and other external verification

What Quote Accuracy Verification Actually Means

Quote accuracy verification is the process by which a comparison service attempts to ensure the price and coverage it displays actually matches what the insurer would charge in a real policy. In practice, most platforms only produce preliminary estimates, not verified, bindable quotes.

The distinction matters:

| Quote Type | What It Means |

|---|---|

| Preliminary quote | Fast estimate based on limited inputs from a web form |

| Verified, bindable quote | Price confirmed after full underwriting and external data checks |

Denmark's Forsikringsguiden explicitly states: "You do not get an insurance offer, but an overview of prices, coverage, and insurance terms." That said, participating companies are obligated to honor the displayed price if you submit identical information when contacting them directly.

This is stronger consumer protection than many commercial platforms offer — but it still hinges on complete accuracy in your initial input.

In Italy's regulatory model, estimates are binding on insurers for 60 days — one of Europe's strongest protections. Denmark sits in a similar position: transparency requirements apply, but there is no universal binding quote standard. For Danish consumers, that means the accuracy of any comparison result depends heavily on how much verified data the platform works with — and what happens after you click.

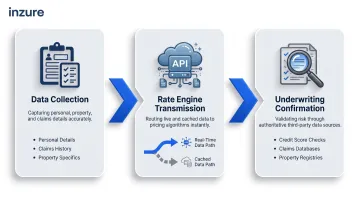

How Insurance Comparison Services Generate and Verify Quotes

Comparison services act as intermediaries, feeding standardised user data into multiple insurers' pricing systems via APIs or direct integrations to retrieve estimated premiums. The process unfolds in three stages.

Step 1: Data Collection From the Consumer

The first step is collecting risk-relevant inputs from you:

- Personal details (age, address, occupation)

- Claims history

- Property specifics (size, construction type, security features)

- Bicycle details (for theft coverage)

- Coverage preferences (deductibles, sum-insured amounts)

The accuracy of these inputs directly determines quote reliability. If you omit past claims, underestimate property value, or forget to mention a partner or child who should be covered, the returned quotes will not reflect what you'd actually pay.

Step 2: Transmission to Insurer Rating Engines

Your data is sent to each insurer's pricing algorithm — their "rate engine" — which applies underwriting rules to generate a premium estimate.

Two transmission methods are used:

- Real-time API connections: Platform queries live insurer systems, receiving current rates instantly

- Cached rate tables: Platform uses stored, averaged data from weeks or months earlier

Nordic insurance rates shifted from hardening (rising above inflation) in 2023-2024 to softening (property rates down 1-10%) in 2025-2026. Cached data from even a quarter ago can overstate premiums by hundreds or thousands of kroner during market transitions.

Top-tier digital insurers have reduced the variance between initial digital quotes and final underwritten prices to less than 5% through better data pre-fill and enrichment. This implies less digitally mature insurers or complex risk profiles see materially higher deviations.

Step 3: Cross-Referencing and Underwriting Confirmation

True quote verification only occurs during underwriting — after you express intent to purchase. The insurer runs external checks not captured in the initial questionnaire:

- Credit scores

- Motor vehicle records

- Claims databases

- Property registries

- Public records

This is where quoted prices most commonly change. The insurer may discover claims you forgot to mention, credit issues affecting your risk profile, or property features requiring higher premiums.

Rather than relying solely on what you remember and enter, Inzure's AI reads and analyses your actual existing policy documents — uploaded as PDFs or photos in 60 seconds. It extracts documented coverage terms, exclusions, deductibles, and pricing, then benchmarks these against real-time market data. This grounds comparisons in verified documentation, not memory, reducing the gap between estimate and final price.

Why Getting Quote Accuracy Right Is Harder Than It Looks

Quote accuracy sounds straightforward — until you look at how comparison platforms actually work. Several structural problems make truly accurate quotes harder to deliver than most platforms admit.

Different Rating Factors Across Insurers

Insurers don't all use the same rating factors or weight them equally. Two insurers assessing identical consumer profiles can arrive at vastly different premiums. Comparison platforms must accurately translate your profile into each insurer's unique rating language — a process prone to error.

Market Coverage Gaps

No comparison platform has access to every insurer on the market. Denmark's Forsikringsguiden covers 86% of the Danish insurance market by premium volume, listing 15 participating insurers including Alka, Alm. Brand, Codan, Gjensidige, Topdanmark, and Tryg. This means 14% of the market is invisible to consumers using this tool alone.

Across Europe, aggregator penetration varies dramatically:

- 53% in Germany

- 48% in the UK

- 36% in France

- 10% in the Netherlands

These gaps aren't accidental. Some major insurers deliberately avoid aggregators to protect brand positioning and sidestep direct price comparisons. The cheapest quote on the market may never appear on any comparison site.

Commission and Revenue Model Problems

Many comparison sites earn revenue from the insurers they list, creating incentives to surface certain insurers over others. This is unlike independent platforms with no insurer affiliations.

Under the EU Insurance Distribution Directive (IDD), comparison websites classified as distributors must disclose:

- Nature of remuneration received (fees, commissions, economic benefits)

- Any 10%+ ownership stakes between platform and insurers

- Names of insurers with contractual relationships

Even with disclosure requirements, the revenue dynamics remain significant. Industry data shows aggregators earn:

- Cost-per-acquisition (CPA) commissions: €40–€125 per policy or 5–15% of premium

- Cost-per-lead (CPL) fees: €12–€37 per lead

- Cost-per-click (CPC) fees: €12–€42+ for high-intent traffic

- Premium placement markups: 15–30% above standard CPC for "Top 3" or "Recommended" spots

Leading European aggregators enjoy EBITDA margins of 30–40%. Products paying the highest commissions may be promoted over products that cost less or better suit your needs.

Inzure's model works differently. The platform charges no referral fees, commissions, or listing fees from insurers at the quote generation or comparison stage. Revenue comes entirely from a 20% commission on savings achieved when customers switch to a better policy through the platform.