Introduction

If you've ever tried to compare two insurance policies side by side, you know the feeling: dozens of pages written in impenetrable jargon, critical exclusions buried in subsections, and formatting so inconsistent it feels like the documents are from entirely different industries. This isn't accidental. Insurance policies have been deliberately designed to be complex, creating a barrier that discourages consumers from questioning what they're paying for or looking elsewhere.

That complexity is exactly what AI cuts through. What used to take hours of careful reading — often ending in confusion rather than clarity — now happens in seconds. AI reads full policy documents, pulls out the terms that actually matter, and flags the differences that affect your wallet and your coverage.

For Danish consumers navigating a market where 70% are concerned about climate change's impact on insurance costs, knowing exactly what your policy covers has never mattered more.

This article explains how AI reviews insurance policy differences, what it looks for, and how it helps you make faster, smarter decisions without becoming an insurance expert yourself.

Key Takeaways

- Manual policy comparison is slow and error-prone — AI cuts through the complexity in seconds

- AI reads complete policy documents, extracts key terms, and surfaces meaningful differences in coverage, pricing, and exclusions

- Analysis that previously required up to 10 hours now completes in under 60 seconds

- No insurance expertise needed — upload your policy and get a plain-language breakdown instantly

- Danish households are saving between 2,800 and 48,000 kr/year by switching based on AI-driven comparisons

Why Insurance Policy Review Is So Hard for Consumers

Insurance policies are structurally unreadable, and the data backs that up. In the US, the National Association of Insurance Commissioners found that a typical homeowners policy runs 69–91 pages and requires 2–3 hours just to read. That's a short novel's worth of content — written in legal language at a reading level most adults can't comfortably parse.

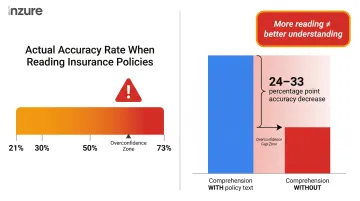

Worse, reading doesn't guarantee understanding. The same study tested 2,440 homeowners using actual policy language and found accuracy rates ranging from just 21% to 73% depending on the scenario.

In two out of seven tested scenarios, having the policy text actually decreased accuracy by 24–33 percentage points compared to guessing without it. Most respondents reported higher confidence after reading — even when their answers were objectively wrong. That overconfidence gap is where real financial harm happens.

The Real Pain Points

Danish consumers face several specific challenges when reviewing insurance policies:

- Indecipherable language: Terms like excess, named perils, and exclusion clauses appear throughout — with no plain-language translation

- Hidden exclusions: Critical coverage limits are buried deep in documents with no clear signposting or summary

- Duplicate coverage: Many consumers pay twice for the same protection without knowing — travel insurance bundled into home contents policies is a common example

- Loyalty penalties: Long-term customers typically pay around DKK 2,400 more annually than new customers for identical coverage, through gradual renewal increases

- Missing coverage: Gaps in protection often go unnoticed until a claim is denied

The financial cost is substantial. In the UK, the Financial Conduct Authority found that in 2018, 6 million customers were overcharged a combined £1.2 billion through loyalty penalty pricing alone. The Danish market operates under the same dynamic — and climate-related coverage concerns have since added another layer of complexity consumers weren't expecting to navigate.

What AI Actually Does When It Reviews an Insurance Policy

AI-powered policy review starts the moment you upload your document. The system accepts any format — PDF, photo, or screenshot — and reads the complete policy, understanding its structure: coverage sections, exclusions, limits, deductibles, and terms.

How Natural Language Processing Works

Natural Language Processing (NLP) allows AI to extract meaning from insurance-specific language, not just recognize words. The system understands what "excess," "exclusion clause," or "named perils" actually mean in context and how they affect your coverage. Purpose-built insurance AI models report 93% accuracy when extracting and interpreting policy documents, significantly outperforming general-purpose language models.

Approximately 62% of consumers accept AI being used to translate policy wording into simpler language, and 80% are comfortable with AI processing insurance documents if it delivers faster outcomes.

Field Extraction and Data Organization

AI pulls out the key data points that matter:

- Premium amounts and payment schedules

- Coverage limits and sub-limits

- Policy duration and renewal terms

- Included and excluded perils

- Add-ons and endorsements

- Deductibles and excess amounts

This information is organized into a readable format that lets you see at a glance what you're actually paying for. Inzure's platform, for example, completes this full analysis in approximately 60 seconds—transforming hours of manual work into an instant overview.

Cross-Referencing and Comparison

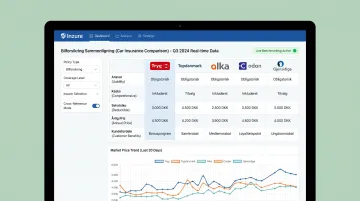

The AI cross-references extracted data against market benchmarks or a second policy to identify where differences exist. For Danish consumers, this means comparing your current coverage against real-time data from Tryg, Topdanmark, Alka, Codan, GF, Alm. Brand, and other providers. The result is a clear picture of not just what your policy says, but how it compares to what you could have at the same price — or less.

AI doesn't replace your judgment here. It surfaces the information so you, or a human advisor, can make an informed decision without wading through 40 pages of fine print.

How AI Identifies Policy Differences That Matter

Not all policy differences are created equal. AI's primary value is its ability to triage: surfacing only the differences that meaningfully affect your coverage or cost, not every minor variation in legal wording.

Coverage Gaps

AI identifies where you're exposed to risk your current policy doesn't cover. Common gaps Danish consumers have found include:

- Burst pipe water damage excluded while comparable plans include it

- Missing bicycle theft coverage for high-value e-bikes

- Inadequate sum-insured limits for valuables

- No legal aid protection despite years of continuous renewal

Duplicate Coverage Detection

Many consumers hold multiple policies—home, contents, travel, accident—that overlap in certain areas. AI maps coverage across all your policies and flags where you're paying twice for the same protection. Common duplicates include:

- Travel insurance already covered by credit cards or the Danish public health card for EU travel

- Accident coverage that overlaps between travel and standalone accident policies

- Legal aid insurance bundled with home contents insurance and purchased separately

Pricing Discrepancies

AI compares your premium against real market pricing for equivalent coverage, identifying when you're being penalized for loyalty. The UK FCA found that contents-only insurance customers with 5+ years of tenure paid approximately 146% more than new customers. While the UK banned dual pricing in 2022, no equivalent prohibition exists at EU level—making Danish consumers vulnerable to the same practice.

Silent Changes at Renewal

AI highlights exactly what changed between your current and previous policy versions. When insurers quietly modify terms at renewal, these changes often cut coverage without warning. Sweden requires insurers to document changes in writing; Denmark has no equivalent rule, so the burden falls entirely on you to spot them.

How AI Speeds Up Decision-Making and Switching

The primary bottleneck in switching insurance isn't cost—it's cognitive effort. Research on Danish consumer behavior found that 96.2% of consumers who could save at least DKK 696 per year remained inactive. Among those who did switch, 78% reported it took less than 15 minutes. The barriers were procrastination (18%) and distrust (18%), not complexity.

AI removes that cognitive barrier by turning hours of document review into a single, readable summary.

Plain-Language Summaries Replace Document Reading

AI-generated summaries give you a clear overview of:

- What you currently have

- What you're missing

- What a competing policy offers differently

- Whether you're overpaying

Instead of comparing two 30-page documents, you read a one-page breakdown organized by coverage category, with specific recommendations for addressing gaps, overlaps, or pricing discrepancies.

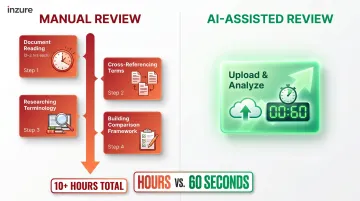

Speed Comparison: Hours to Seconds

Manual policy comparison involves several time-consuming steps:

- Reading multiple documents (2-3 hours each)

- Cross-referencing terms and exclusions across policies

- Researching unfamiliar insurance terminology

- Building a mental or spreadsheet comparison framework

Total time investment: typically 10+ hours for complete analysis.

AI-assisted review: under 60 seconds for complete analysis with market context. Platforms like Inzure deliver full policy breakdowns, coverage gap identification, and market pricing benchmarks in the time it takes to upload your documents.

Clarity Drives Action

When you can see clearly that you're overpaying by thousands of DKK annually—or that your family members aren't covered despite assumptions otherwise—the decision to update or switch becomes straightforward rather than overwhelming. Danish consumers using AI analysis have documented savings from DKK 2,800 to DKK 48,000 annually. That money was always available. Most people just never had the information to act on it.

What to Look for in an AI Insurance Review Tool

Not all AI insurance platforms are created equal. When choosing a tool to analyze your policies, prioritize these critical factors:

Independence from Insurers

Independence is the single most important factor. The AI platform should have no financial relationship with any insurance company — a tool built or funded by an insurer has a built-in conflict of interest and may quietly filter out alternatives that benefit you rather than them.

Inzure operates with no carrier affiliations, analyzing policies across Tryg, Alka, Topdanmark, and others without a financial stake in where you land. Denmark's Insurance Guide (forsikringsguiden.dk), run jointly by Insurance & Pension Denmark and Forbrugerradet Tænk, covers 86% of the market — but it's an industry collaboration, not a consumer-first AI tool built to challenge carrier pricing.

Data Privacy and GDPR Compliance

You're uploading sensitive financial documents, so GDPR compliance and secure EU data storage are non-negotiable. Verify that the platform:

- Stores data on EU servers

- Clearly discloses who has access to uploaded documents

- Provides transparency on data retention periods

- Allows you to withdraw consent or delete data at any time

According to Deloitte's insurance AI research, approximately 41% of consumers are concerned about how AI platforms handle their data — which means a platform that can't answer these questions clearly isn't one you should trust with your policies.

Transparency of Output

Look for platforms that explain what they found and why it matters in plain language — not just a score or a vague recommendation. Useful output includes:

- Specific breakdowns of coverage gaps, overlaps, and pricing differences

- Clear comparisons against market benchmarks

- Actionable next steps with no obligation to switch

- Explanations of how each finding was determined

A tool that can't show its reasoning offers little advantage over calling your broker.

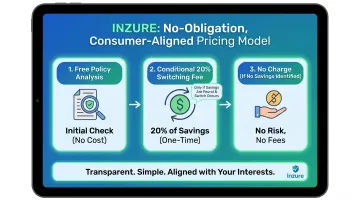

No Obligation and Clear Pricing

Free analysis should be the baseline — you shouldn't pay to find out what you're paying too much for. Inzure's model works as follows:

- Policy analysis: Always free

- Switching fee: 20% of annual savings, charged only if a better deal is found and you switch

- No savings found: No charge, no obligation

If you switch for better coverage at the same price, that's also free. The fee structure is designed so Inzure only earns when you do.

Frequently Asked Questions

Can AI compare two insurance policies?

Yes. AI reads your uploaded policy and extracts key terms, then flags differences in coverage, limits, exclusions, and pricing against market benchmarks. The result is clear visibility into what differs and what it costs you.

How accurate is AI at reading insurance policy documents?

Modern AI using Natural Language Processing achieves high accuracy in extracting structured data from insurance documents. Purpose-built insurance AI models report 93%+ accuracy for policy extraction, though accuracy depends on whether the model was trained on insurance language or general text.

How long does it take AI to review an insurance policy?

AI completes a full policy analysis in under 60 seconds, compared to 2-3 hours for manual reading of a single policy and 10+ hours for thorough comparison across multiple providers. This makes it practical to run checks regularly, not just at renewal time.

What types of policy differences can AI identify?

AI identifies four main issues: coverage gaps you're missing, duplicate coverage across multiple policies, pricing discrepancies versus market rates, and silent changes between policy versions at renewal. Only meaningful differences get flagged — not every minor variation.

Is my personal insurance data safe when using AI tools?

Look for platforms that store data within the EU under GDPR compliance — this is a baseline, not a bonus. Before uploading any documents, check where data is stored, who can access it, how long it's retained, and whether you can request deletion.

Can AI replace an insurance advisor?

AI handles the reading and comparison work; you still make the final call. It turns 40 pages of legal text into a clear summary, removing the information gap — but your specific circumstances, risk tolerance, and coverage priorities still require human judgment.